Uber Reality Check: Surge Ended

Uber reported $6.9B net income—but only $770M was real. With Tesla's Cybercab targeting $0.50/mile and the CEO dumping shares, the 'cheap' P/E is a mirage.

You are holding $UBER at $74 telling yourself it's a growth stock, but let's be honest: you are actually clutching a potential value trap. It hurts, I know, but we need to stop the bleeding before the Tesla infection spreads and your portfolio flatlines.

The Diagnosis

Verdict: Value Trap / Technological Obsolescence Risk

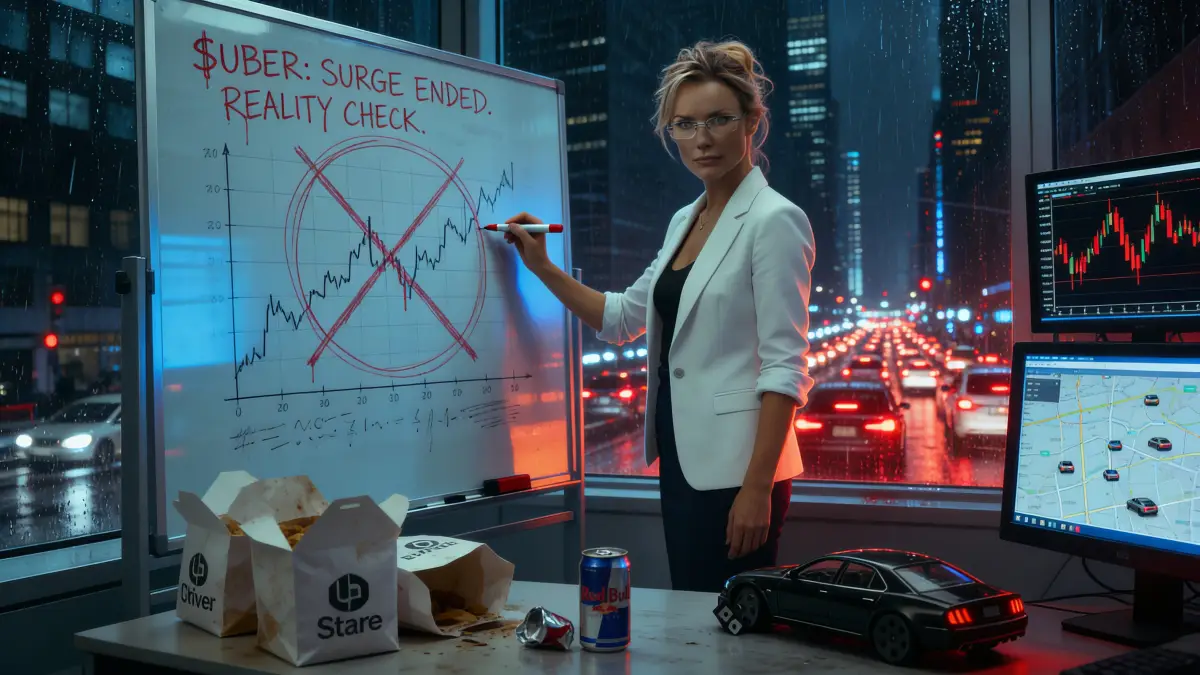

As of Feb 7, 2026, post-earnings, $UBER appears to be suffering from a classic "Wile E. Coyote" moment—running off the cliff of technological obsolescence without looking down. While the stock hovers around $74.77, forensic analysis suggests this level is less of a "floor" and more of a liquidity exit for institutional capital. Key risk: a massive divergence between reported Net Income and actual Operating Income, suggesting the "cheap" valuation is a dangerous mirage.

The Vitals

| Metric | Value | Signal |

|---|---|---|

| Revenue | $14.4B (+18% YoY) | Healthy |

| Operating Income | $770M (vs $6.9B reported NI) | Mirage |

| Insider Selling | CEO sold 450k shares (~$63M) | Bearish |

| Valuation | 9.4x P/E (distorted by equity gains) | Deceptive |

The Pathology

1. The "Fake" Earnings Facade

The Fact: $6.1 billion of Uber's reported Q4 Net Income comes from "unrealized gains" on equity stakes (Aurora, Grab, etc.).

This is "paper money," darling. It cannot fund buybacks or pay dividends. Investors screening for a low P/E are seeing a ghost. The real operating P/E is likely closer to 30x-45x. You are paying a premium for a holding company masquerading as a tech giant.

2. Squeezed by Elon and Europe

The Fact: Tesla's Cybercab is targeting operating costs of under $0.50/mile (vs. Uber's ~$2.50), while the EU Platform Work Directive (2026) threatens to hike labor costs by 20-30%.

Uber is fighting a deflationary war with robots and an inflationary war with regulators simultaneously. If Tesla undercuts Uber by 50%, the network effect liquidity—your primary bull thesis—could drain overnight.

The Steel-Man (Bull Case)

Now, I know why you like her. She's seductive.

If the "Marriott Model" works—where Uber becomes the manager for AV fleets (Waymo, Cruise) rather than the owner—that 202 million user base makes them an indispensable utility. With $9.8 billion in Free Cash Flow and a $20 billion buyback, the company has a massive war chest to defend the stock price.

If AVs stall, Uber remains the monopoly. But betting on your competitor's failure is not a strategy—it's a prayer.

Nurse's Orders

1. Watch the $73 Support Level

Technicals show a "bull trap" at $80. If the price breaks strictly below $73, look for a "technical air pocket" that could see the stock re-rate down to the $60-$65 range. That gap has gravity.

2. Monitor Insider Activity

When the CEO sells 450,000 shares and the CFO leaves immediately after a "record" quarter, retail investors should ask: What do they know that I don't? Zero insider buying against $63M in selling is not a confidence signal.

3. Wait for the Washout

A valuation of ~12x FCF (approx. $60/share) historically provides a margin of safety. Entering before the washout may be catching a falling knife. Patience pays more than conviction in a value trap.

Bottom Line

The real operating P/E is 30-45x, not the 9.4x on your screener. Wait for the washout to $60 before you even think about buying the dip.